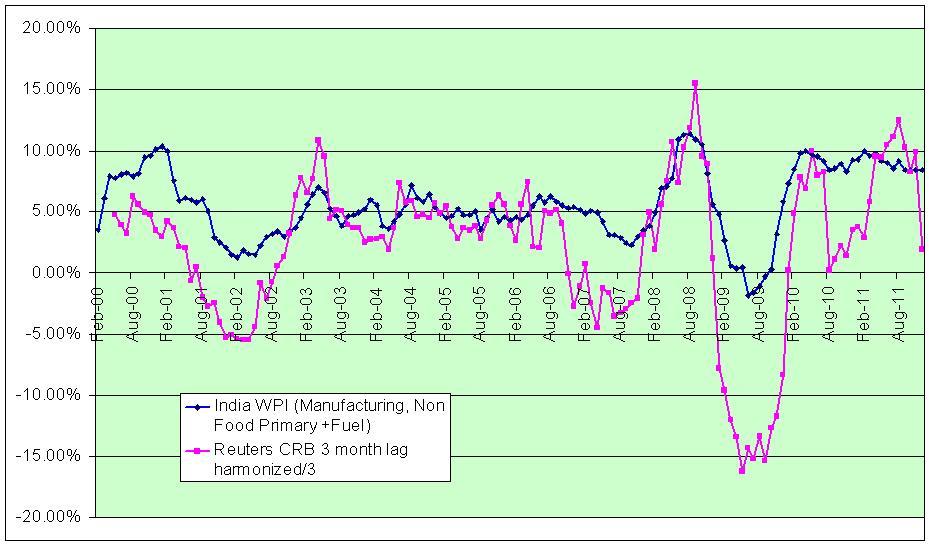

As a follow up to my article written a few weeks back I am now writing this article which will further prove that Indian WPI inflation is largely driven by global commodity prices with a lag. Although the earlier article did prove that RBI policies are totally ineffective in controlling inflation while restricting investment demand and growth. The current analysis also shows the same effect.

For the purpose of the analysis I have attempted to see the impact of the movement of Reuters CRB index and have tried to correlate it with Indian WPI inflation.

– In my first iteration I just took the WPI figures as they are over the last 12 years and did a correlation with the Reuters CRB Index on a like to like basis. This correlation did work well however there was a lag impact that was apparent.

-Secondly I did an analysis of the WPI with the Reuters CRB Index taking a 3 month lag i.e. the impact of the movement of global commodity prices is felt in India

Thirdly in order to further refine the study I broke up India

As such given the fact that the Reuters CRB Index has crashed by over 15% in the month of September 2011 the impact of this on the WPI inflation will be seen clearly by December. Inflation will fall much faster than being currently estimated and given the way global commodities have corrected we could be at a 5.5% figure by March 2012.

Without reiterating the points that I made in my previous article this analysis further proves the ineffectiveness of RBI policies on inflation in an globalized world with low customs duties and free trade. It is time to focus on growth in the domestic economy as the global growth falters

Markets

The month of September was another tough one for global markets with the sell off that started in a big way in August continuing during the start of the month before the markets started to stabilize by the second week of the month. Most Western markets ended up with losses of around 4-5% and the Indian markets were down by around 1.5%. The key feature of the month however was not the movement in the stock markets but in the forex, commodity and bond markets. The Euro crisis along with the extreme scare in global markets created an artificial global shortage of Dollars with most banks refusing to take counter party risks and a significant pull back of money by US Banks, Funds, and Investors etc in the US

Most global commodities corrected sharply during the month with copper seeing one of the most massive falls of around 25%, Crude fell by over 12% and most other Industrial and agricultural commodities corrected similarly and the Reuters CRB Index ended with losses of 13% for the month. Commodity speculators were holding on to their speculative position in the hope of QE3 and as that got dashed with the commentary that came along with “Operation Twist” of the US FED there was a massive outflow out of commodity long positions in the last 10 days of the month. Although we have seen a cut in long position, there is yet to be a sharp outflow out of commodity funds which should happen over the next couple of months and further pressurize commodity prices. With the duration of Operation Twist being till May 2012 and hopes of QE3 will be only after that.

The Euro zone crisis continued during the month and despite all the reassuring words most people believe that Greece

The bond markets also saw huge movements with the bonds of troubled Euro countries again getting sold off and the rally in US and German bonds continued for the month. Yields on US 10 year bonds fell from 2.23% at the end of August to as low as 1.67% before ending the month at 1.92%.

Gold prices saw a massive sell off during the month as there was no QE3 and investors decided to book some profits in one of the only performing assets. The correction seems to have some more legs to go and we could see the correction continue to $ 1450 levels at the first instance and maybe to $ 1300 over the next few months.

On an overall basis taking into account the panic in the markets as reflected in volatility indices, overbought positions of Bunds and the US Govt Bonds, massive outflows out of Equity Funds globally etc. it looks like we are more near the bottom of the markets than there being any possibility of a massive selloff in equities. The key in my view is whether we have a “Lehman Moment” or not. If we do not then we should have made a low for 2011 for the equity markets globally and will see a recovery in this quarter.

As far as the domestic scenario goes the industrial production data surprised on the downside and inflation was in line with expectations. There was some movement from the government on the policy front but there is a lot that needs to be done on that front. Whether India

Overall l am looking t

owards the last quarter of the year constructively as one of the major concerns forIndia

owards the last quarter of the year constructively as one of the major concerns for

In a nutshell my guess is that we have a worst case downside of 8-10% with an upside potential of 25-30% over the next one year.