Over the last few days there has been an increased clamor for controlling the Fiscal Deficit by increasing taxes in the forthcoming Union Budget. In my view raising taxes in a slowing economy is a retrograde step that will create further headwinds for the economy and slow down growth. Indirect tax increases are also inflationary in nature and given the fact that

We have seen that in a large number of Euro zone countries that are facing financial troubles the panacea for all ills has been proposed to be increased austerity and higher taxes to reduce the fiscal deficit. However in reality we have seen that a combination of reduced money velocity, deleveraging and higher taxes lower expenditure has infact led to countries missing their Fiscal Deficit goals as the denominator itself has shrunk (i.e. the GDP). On the other hand a combination of extremely benign liquidity provided by the US Federal Reserve combined with a still high Fiscal Deficit has stabilized the situation in the USA

Nevertheless the Euro situation is a topic in itself. More important is to look at what the government should be doing. Given the fact that the currency has stabilized and inflation is clearly on the way down, it is important to now focus on growth from both the monetary and fiscal angles. From the fiscal side it essentially means not increasing taxes at this stage. RBI obviously needs to cut aggressively. The government needs to focus on cutting subsidies, pursuing reforms and taking a better stock of expenditure under schemes like NREGA where not much capital formation seems to be taking place. Government measures need to be counter cyclical. Once growth has clearly revived and things are on a more assured path that will be the time to actually take harsher measures on cutting Fiscal Deficits and creating a buffer for the next downturn.

Results

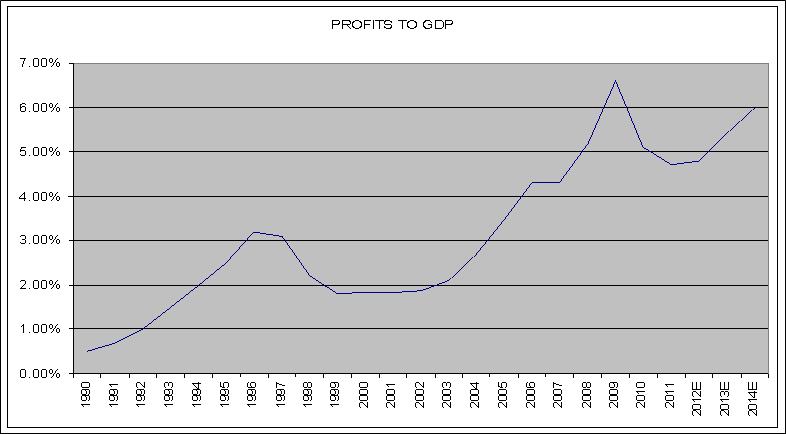

Company results that have come out till date have largely been in line with expectations and in most cases have held on pretty well. Topline growth for the companies that have reported till date have been nearly 27% with a profit growth of 6%. Margins have come down on the operating front mainly due to a lagged impact of higher input costs. Also interest costs of companies in general have gone up sharply due to both higher rates and longer debtor cycles or lower creditor cycles. The last two years have been ones of margin compression in India

The Elliot Wave Theory

Although I am personally not a big believer in Elliot waves, mainly due to the amount of exceptions and variables involved the psychology of Elliot Waves is very interesting and reflects market psychology. As you read through Wave 1 you will realize how true it is to the current market psychology.

|

Five wave pattern (dominant trend)

|

Three wave pattern (corrective trend)

|

|

|

Wave 1: Wave one is rarely obvious at its inception. When the first wave of a new bull market begins, the fundamental news is almost universally negative. The previous trend is considered still strongly in force. Fundamental analysts continue to revise their earnings estimates lower; the economy probably does not look strong. Sentiment surveys are decidedly bearish, put options are in vogue, and implied volatility in the options market is high. Volume might increase a bit as prices rise, but not by enough to alert many technical analysts.

|

Wave A: Corrections are typically harder to identify than impulse moves. In wave A of a bear market, the fundamental news is usually still positive. Most analysts see the drop as a correction in a still-active bull market. Some technical indicators that accompany wave A include increased volume, rising implied volatility in the options markets and possibly a turn higher in open interest in related futures markets.

|

|

|

Wave 2: Wave two corrects wave one, but can never extend beyond the starting point of wave one. Typically, the news is still bad. As prices retest the prior low, bearish sentiment quickly builds, and “the crowd” haughtily reminds all that the bear market is still deeply ensconced. Still, some positive signs appear for those who are looking: volume should be lower during wave two than during wave one, prices usually do not retrace more than 61.8% (see Fibonacci section below) of the wave one gains, and prices should fall in a three wave pattern.

|

Wave B: Prices reverse higher, which many see as a resumption of the now long-gone bull market. Those familiar with classical technical analysis may see the peak as the right shoulder of a head and shoulders reversal pattern. The volume during wave B should be lower than in wave A. By this point, fundamentals are probably no longer improving, but they most likely have not yet turned negative.

|

|

|

Wave 3:

Wave three is usually the largest and most powerful wave in a trend (although some research suggests that in commodity markets, wave five is the largest). The news is now positive and fundamental analysts start to raise earnings estimates. Prices rise quickly, corrections are short-lived and shallow. Anyone looking to “get in on a pullback” will likely miss the boat. As wave three starts, the news is probably still bearish, and most market players remain negative; but by wave three’s midpoint, “the crowd” will often join the new bullish trend. Wave three often extends wave one by a ratio of 1.618:1. |

Wave C: Prices move impulsively lower in five waves. Volume picks up, and by the third leg of wave C, almost everyone realizes that a bear market is firmly entrenched. Wave C is typically at least as large as wave A and often extends to 1.618 times wave A or beyond.

|

|

|

Wave 4: Wave four is typically clearly corrective. Prices may meander sideways for an extended period, and wave four typically retraces less than 38.2% of wave three (see Fibonacci relationships below). Volume is well below than that of wave three. This is a good place to buy a pull back if you understand the potential ahead for wave 5. Still, fourth waves are often frustrating because of their lack of progress in the larger trend.

|

||

|

Wave 5: Wave five is the final leg in the direction of the dominant trend. The news is almost universally positive and everyone is bullish. Unfortunately, this is when many average investors finally buy in, right before the top. Volume is often lower in wave five than in wave three, and many momentum indicators start to show divergences (prices reach a new high but the indicators do not reach a new peak). At the end of a major bull market, bears may very well be ridiculed (recall how forecasts for a top in the stock market during 2000 were received).

|

||

Markets

Stock markets have behaved as per expectations this year and have shown a strong up move. In all probability a new bull phase has started in the midst of extreme pessimism. The markets have moved up by nearly 15% since the beginning of the month. Momentum can carry the markets forward after which we could see a correction that is short and swift. Most people have been left out in this move and are waiting on the sidelines for an opportunity to move into the markets. The cash on the sidelines is quite substantial and in terms of asset allocation equities are at very low levels. Specific to India most global investors were heavily underweight India IRAN