The continued rally in the bonds of developed markets like US, Germany US US UK and Germany US Italy

This has happened in combination with the continuous up move in key global stock markets where US & German markets are now at all time highs and a number of other markets are at multiyear highs. A market like Japan India

Data actually suggests that the great rotation has not yet started in any big way. There is not much sign of money moving from bonds to equities, although incrementally equities are getting money now. The key is that low interest rates have been one of the major reasons for the revival in the US US

Now if we go back to the last bull phase in equities we see that the bond yields went up from 3.1% in the year 2003 (when the bull phase started) to a level of around 5.2% till the third quarter of the year 2007. As such the move was around 2% from top to bottom. A similar move should happen over the next few quarters where the bond yields should move to the upper end of the channel. Normally such moves are accompanied by strong equity market rallies; let’s see how it plays out this time.

MID MONTH MARKET UPDATE

The first move where I had expected that the US and German markets will move to all time highs has fructified. As per a latest survey of fund managers it has been found that the overweight position on EM’s is very low and most investors have concentrated on DM’s. A shift in interest is imminent going forward and we should in all probability see Emerging Markets outperform over the course of the remainder of the year 2013. Obviously it does not mean that there will be no volatility, there should be bouts of volatility in between. The DOW is up 16%, DAX 9.5% & FTSE 13% YTD. Most BRIC’s markets are either flat, down or marginally up in the same time period. As credit conditions become benign & risk taking increases we will see money move more into second tier markets.

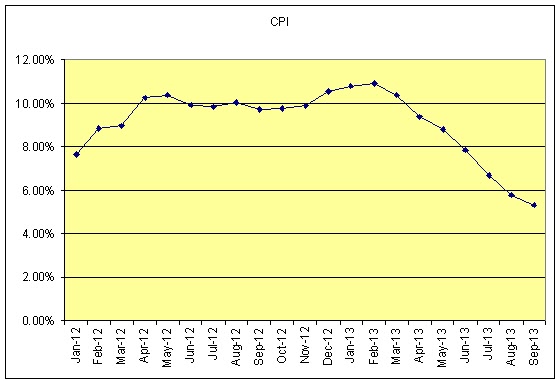

In the Indian context the results season has been reasonably good relative to the extremely low expectations that were built up. As I had expected the WPI inflation has collapsed and will remain subdued for an extended period of time. The moderation in CPI has just started and we should see levels of 7% by July and 5.5% by September.

Contrary to RBI commentary, they will be forced to loosen monetary policy significantly. This in turn will be extremely positive for the revival of the economy as well as corporate earnings growth. The moderation in input costs has already had a positive impact on company margins, but for the operating leverage to come in we also need a revival in the economy that will boost the topline. The revival of the investment cycle requires more action from the government, the progress of which will be keenly watched. As such my base case assumption of a 15% return in the year 2013 seems to be on track. Upsides will depend on government action.