The month of August started off with reasonable optimism backed by both domestic and international factors. On the domestic front the pick up in the Monsoon rains, lower than reported inflation data as well as an anticipation of some economy friendly measures from the government continued to support the markets. Internationally positive data points from the US economy combined with the promise of the European Central Bank to “do what it takes” in order to bring some support to the Eurozone were supportive of the markets. However by the end of the month the issues related to the Coal Mining Allocations & lack of any policy action from the government on the domestic front and doubts about the further actions that the US Federal Reserve or the ECB would take created doubts in the minds of the markets which lead to profit booking coming back to the markets.

The broader markets underperformed as the market interest continued to be in a few large cap and defensive mid cap names. Foreign Funds (FIIs) continued to put money into the Indian markets driven by India India

The major reason for broader markets underperformance continues to be high interest rates that are taking a toll more on the relatively smaller corporates as well as the fact that domestic money flow into the markets continues to be negative. Normally smaller companies are invested into by domestic investors initially and at later stages of a bull market the global investors come in.

There seems to be a consensus in the markets building up that the month of September will be tough for the markets and there could be a significant sell off. As a result we have seen investors become wary lately. Normally consensus does not work so let’s see.

Bernanke and Draghi

The month of September will also be very important for the markets due to two reasons. The first being the fact that the Europeans will be coming back from vacation and the Euro Crisis will again be in focus. The actions of the ECB will need careful monitoring. Incase they are able to bring about a mechanism to control the yields on Italian and Spanish bonds we could see global markets including India

From the domestic perspective the data point of importance will be the inflation figures for August which should see a decent moderation from last month. This could set the tone for monetary easing and set the tone for a significant market rally. The global markets are in a situation today where the global Market Capitalization/GDP is at around 100% and for India India due to higher input costs and interest rates whereas in countries like the US

The end of the month also saw the Shome panel deliver its report on GAAR as well as other aspects of taxing capital gains and capital flows. The recommendations are extremely progressive and if implemented fully would lead to an increase in capital flows into the country and also reduce tax litigation substantially. By removing artificial taxation different ions it could boost the domestic Fund Management industry substantially. Today lots of Fund Managers handling offshore India money sit in places like Singapore and Hong Kong . Implementation of these recommendations could make management of funds independent of the place in which the fund manager sits, which should have been the scenario in any case. This could actually, over a period of time make India

Some Interesting Statistics

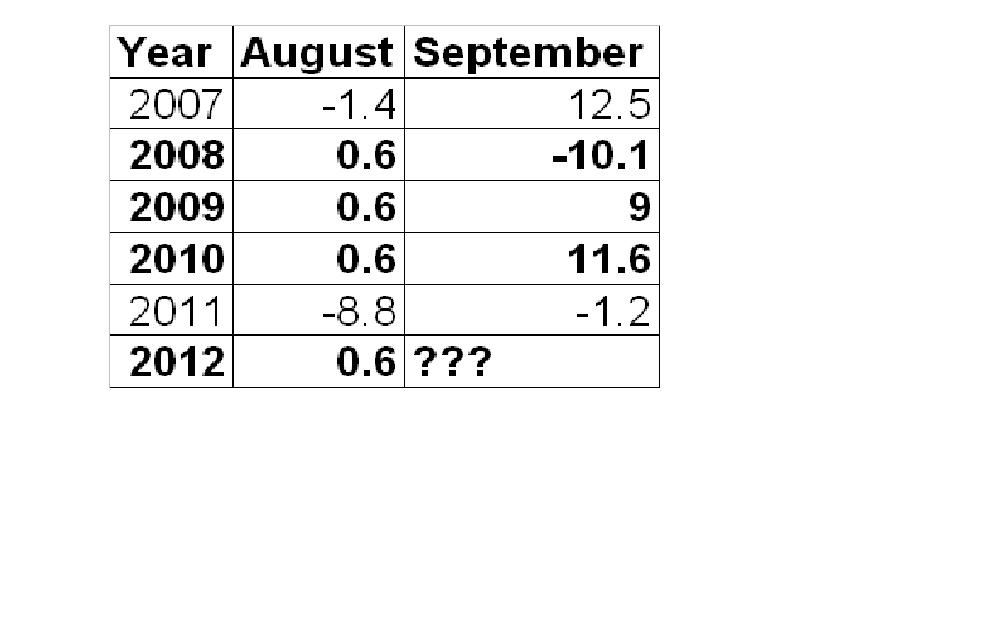

The last five to six years show some very interesting statistics. In 4 out of the last 5 years the month of August has been pretty subdued (at least on headlines) for the markets and the amazing part is that the markets have given a return of exactly 0.6% in these 4 years. The only exception was the year 2011 when the markets fell by 8.8% August. In all these years the month of September has been extremely dynamic except for the year 2011 when September was subdued. The only year when the markets actually sold off in the month of September during this phase was in the year 2008 when September was the Lehman month. The table below illustrates this phenomenon.

The last week of August also saw the markets correct with a substantial reduction in the Put/Call ratio in the derivative markets thus reflecting negative trader sentiments. This shows that the month has started with more short positions than longs. So could we have a repetition of 2007,2009,2010 this year ? Only time will tell.